Conceptually, the contribution margin ratio reveals essential information about a manager’s ability to control costs. The contribution margin may also be expressed as a percentage of sales. When the contribution margin is expressed as a percentage of sales, it is called the contribution margin ratio or profit-volume ratio (P/V ratio). For this section of the exercise, the key takeaway is that the CM requires matching the revenue from the sale of a specific product line, along with coinciding variable costs for that particular product. The contribution margin (CM) is the profit generated once variable costs have been deducted from revenue. This is the net amount that the company expects to receive from its total sales.

Operating Assumptions

The contribution margin shows how much additional revenue is generated by making each additional unit of a product after the company has reached the breakeven point. In other words, it measures how much money each additional sale «contributes» to the company’s total profits. Where C is the contribution margin, R is the total revenue, and V represents variable costs. It represents the incremental money generated for each product/unit sold after deducting the variable portion of the firm’s costs. The contribution margin is the amount of revenue in excess of variable costs.

Do you own a business?

Such fixed costs are not considered in the contribution margin calculations. You might wonder why a company would trade variable costs for fixed costs. One reason might be to meet company goals, such as gaining market share.

- Fixed costs stay the same regardless of the number of units sold, while variable costs change per unit sold.

- As we said earlier, variable costs have a direct relationship with production levels.

- The difference between the selling price and variable cost is a contribution, which may also be known as gross margin.

- The contribution margin is affected by the variable costs of producing a product and the product’s selling price.

Contribution Margin vs. Gross Profit Margin

Next, the CM ratio can be calculated by dividing the amount from the prior step by the price per unit. We’ll next calculate the contribution margin and CM ratio in each of the projected periods in the final step. The insights derived post-analysis can determine the optimal pricing per product based on the implied incremental impact that each potential adjustment could have on its growth profile and profitability. Below is a breakdown of contribution margins in detail, including how to calculate them.

Contribution margin compared to gross profit margin

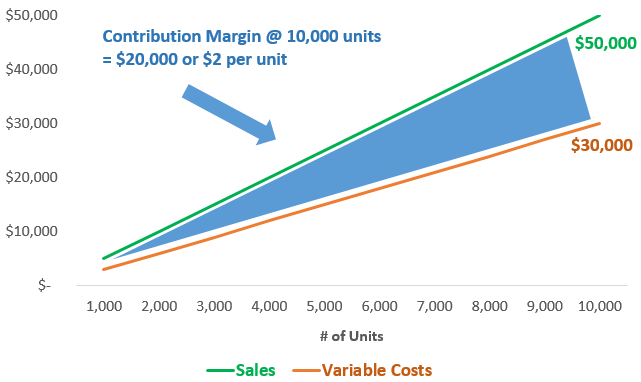

Find out what a contribution margin is, why it is important, and how to calculate it. Thus, at the 5,000 unit level, there is a profit of $20,000 (2,000 units above break-even point x $10). The actual calculation of contribution margin may be more laborious but the concept applies. The contribution margin is given as a currency, while the ratio is presented as a percentage. Variable costs tend to represent expenses such as materials, shipping, and marketing, Companies can reduce these costs by identifying alternatives, such as using cheaper materials or alternative shipping providers.

The contribution margin is affected by the variable costs of producing a product and the product’s selling price. Yes, it means there is more money left over after paying variable costs for paying fixed costs and eventually contributing to profits. However, an ideal contribution margin analysis will cover both fixed and variable cost and help the business calculate the breakeven. A high margin means the profit portion remaining in the business is more.

It is calculated by dividing the contribution margin per unit by the selling price per unit. All you have to do is multiply both the selling price per unit and the variable costs per unit by the number of units you sell, and then subtract the total variable costs from the total selling revenue. The contribution margin is the foundation for break-even analysis used in the overall cost and sales price planning for products.

You can calculate the contribution margin by subtracting the direct variable costs from the sales revenue. Suppose Company A has the following income statement with revenue of 100,000, variable costs of 35,000, and fixed costs of 20,000. The contribution margin helps to easily calculate the amount of revenues left over to cover fixed costs and earn profit.

Profits will equal the number of units sold in excess of 3,000 units multiplied by the unit contribution margin. However, when CM is expressed as a ratio or as a percentage of sales, it provides a sound alternative to the profit ratio. When there’s no way we can know the net sales, we can use the above formula to determine how to calculate the contribution margin. The higher a product’s contribution margin and contribution margin ratio, the more it adds to its overall profit. Fixed costs are often considered sunk costs that once spent cannot be recovered.

To calculate this figure, you start by looking at a traditional income statement and recategorizing all costs as fixed or variable. This is not as straightforward as it sounds, because it’s not always clear which costs fall into each category. Analyzing the contribution how to convert myob to xero margin helps managers make several types of decisions, from whether to add or subtract a product line to how to price a product or service to how to structure sales commissions. Before making any major business decision, you should look at other profit measures as well.

Variable costs refer to costs that change when volume increases or decreases. Some examples include raw materials, delivery costs, hourly labor costs and commissions. It is the monetary value that each hour worked on a machine contributes to paying fixed costs. You work it out by dividing your contribution margin by the number of hours worked on any given machine. The contribution margin may also be expressed as fixed costs plus the amount of profit.

Necesitas Date de alta o Entrar para poder comentar